Perps perps perps

101 and curiosity on perps

It's been a few months since I last published on this newsletter. This was likely due to a mix of weariness and a lack of interesting discoveries to share with you.

That is no longer the case.

Today, I will discuss perpetual protocols. This DeFi vertical has gained momentum over the past four years, and while it is not yet fully mature, it is already a varied and deep market.

We will explore it in three complementary ways:

By discussing Perps 101: What are they? What are they used for?

A snapshot of the market and its main players

By sharing a few "red pills" about the market.

Perps 101

What are perps?

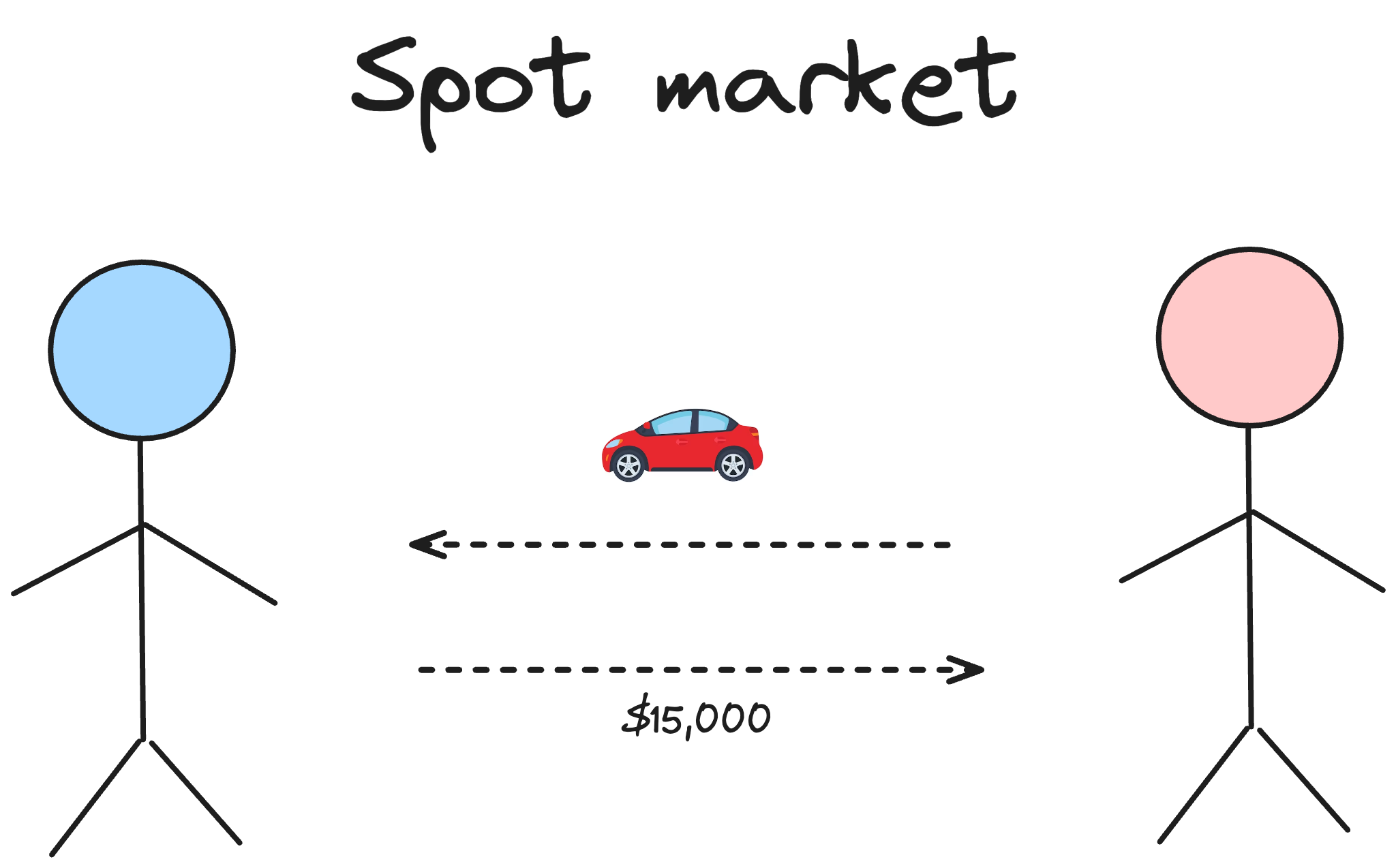

Imagine you and your friend want to trade cars, but instead of just swapping them right away, you decide to play a game where you can keep trading the cars and forth forever. You’re not actually giving away the cars—you’re just betting on whether their value will go up or down, and you can keep doing this as long as you want. That’s kind of how perpetual exchanges work in the world of finance.

In a perpetual exchange, people don’t buy or sell actual things like objects or stocks or crypto; instead, they bet on whether the price of something will rise or fall. And unlike regular trading, there’s no end date—people can keep making those bets for as long as they like.

Now in financial terms, perpetuals refer to a type of derivative contract with no expiration date. Unlike traditional futures contracts that settle on a specific date, perpetuals allow traders to hold positions indefinitely, making them closer in structure to a margin-based spot market.

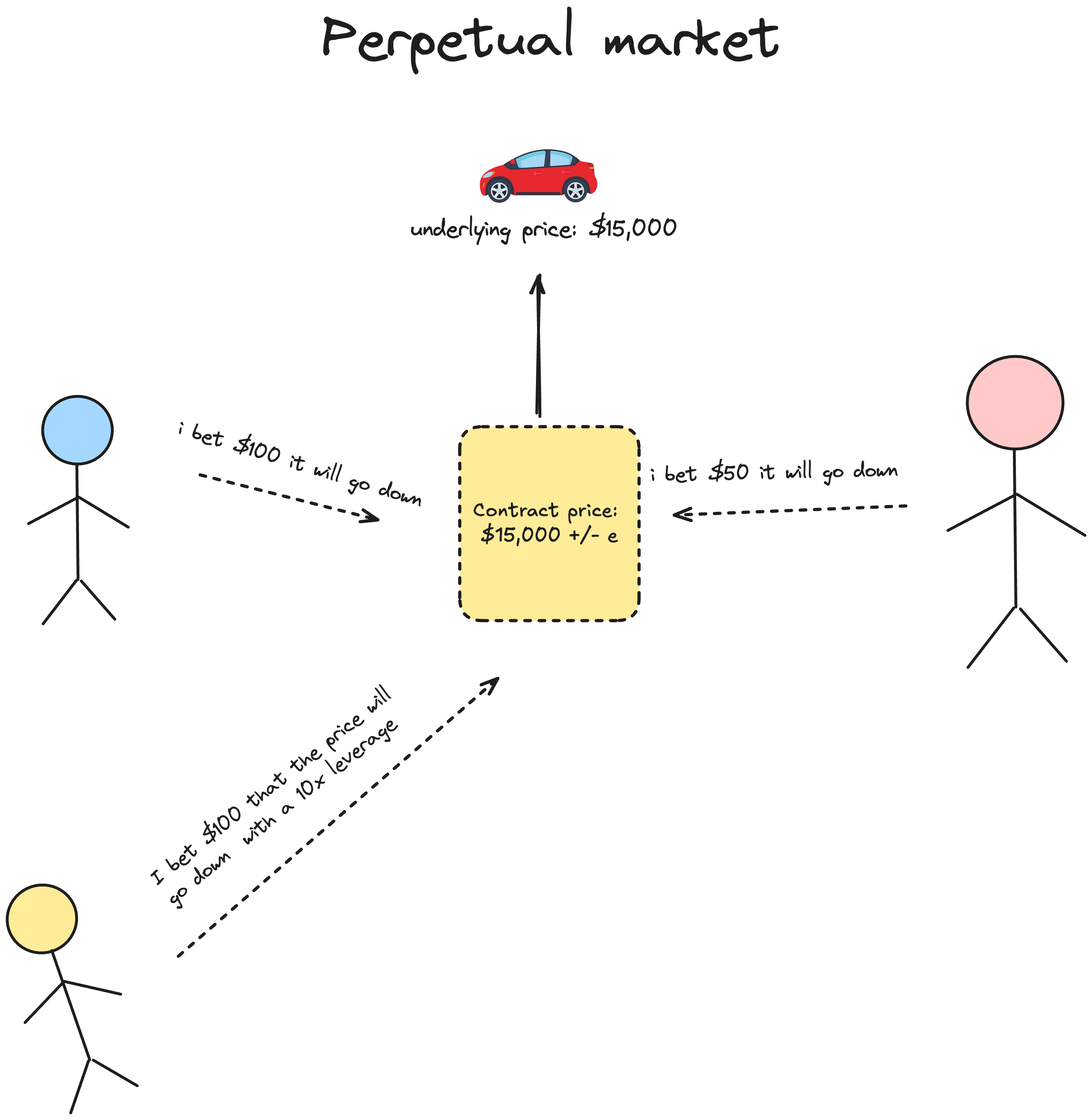

But how the price of the perpetual contract keep being aligned with the spot price? (i.e. underlying asset value)

Getting back to the car example. Thecar has a real price (like what it sells for at the store), but in your game, the price of the car might be a little different because of how people are betting.

The price in your game (contract price) can drift away from the real price (asset price) because everyone’s making bets, and maybe a lot of people think the price will go up, so they push your game’s price higher.

There's something called the funding rate to keep things from getting too far apart. The funding rate is like a rule in your game that helps keep the price in your game close to the real price. If the price of your game gets too high, people who bet it will go up have to pay a little bit to those who bet it will go down, and vice versa. This way, the prices don’t go too crazy, and they stay close to each other!

Why perps are so successful?

Advantages of perpetual contracts are their ability to offer price discovery, leverage, and hedging benefits.

Price Discovery: Imagine the price of Bitcoin on the spot market is $30,000, but on a perpetual exchange, the contract price is $30,500 because lots of traders are betting it will go up. The funding rate will kick in, making it more expensive to hold those bullish bets, which brings the contract price closer to the spot market price. This constant feedback loop keeps prices aligned.

Leverage: Suppose you have $1,000 but want to take a position worth $10,000 on the price of Ethereum. With 10x leverage on a perpetual exchange, you can control that larger position with just your $1,000. If the price moves 5% in your favor, you’d gain $500 (50% of your $1,000), but if it moves against you, you’d lose $500—so gains and losses are magnified.

Hedging: Suppose you own $50,000 worth of Tesla stock and are worried its price might drop. Instead of selling your shares, you can open a short position on a perpetual contract that bets Tesla’s price will fall. If the stock price does drop, your loss in the stock market will be offset by the gain in your short position, protecting your portfolio without having to sell your Tesla shares.

Perps market

Actors

Initially, the perpetual market in crypto developed mainly around centralized players. The most notable examples are Binance, Bybit, OKX, and CEX.io. But today, we’ll focus on their decentralized counterparts (to varying degrees).

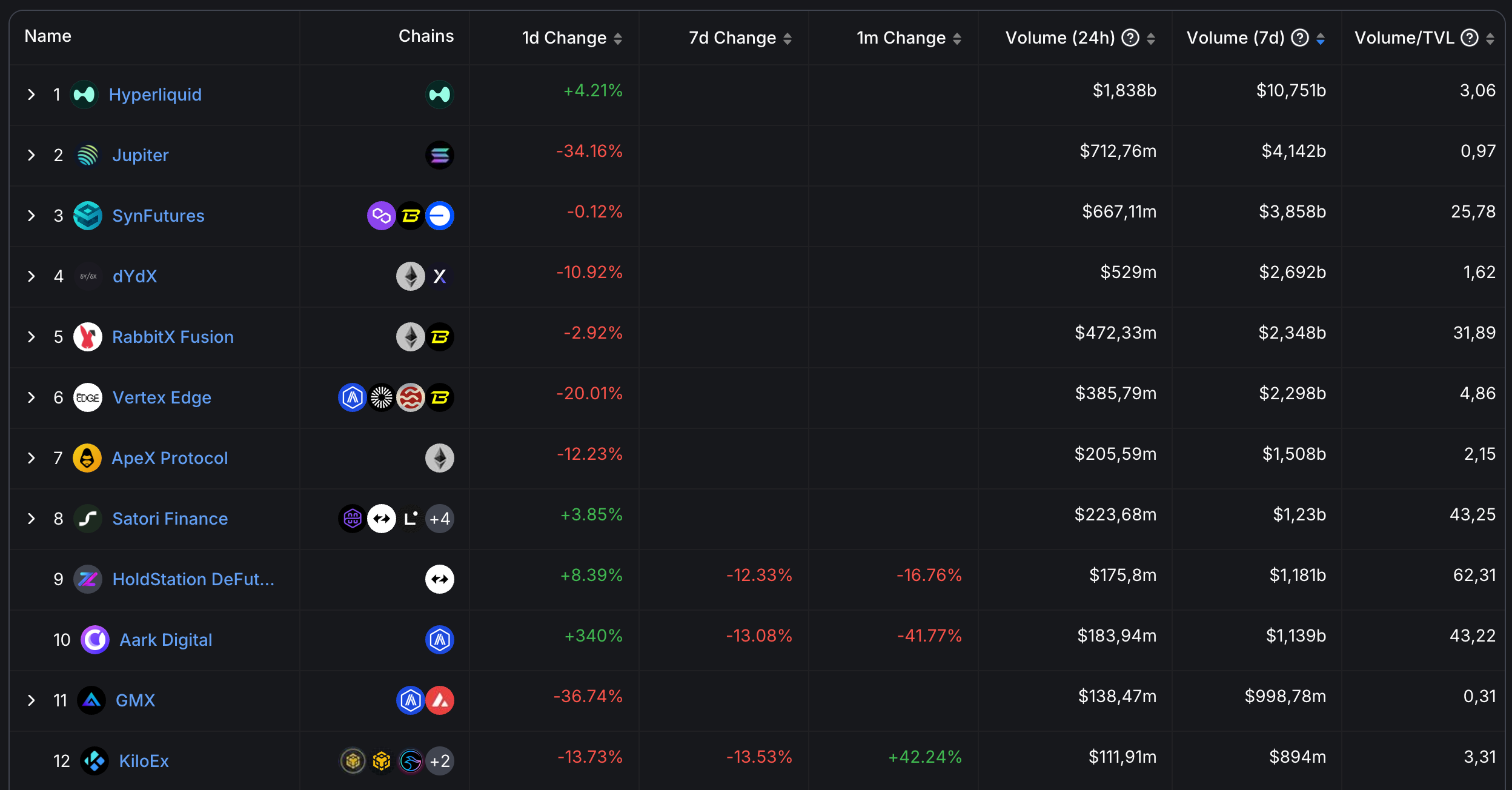

Since 2021 and the pioneers, the ecosystem has seen the emergence of dozens of them. Defillama offers a fairly comprehensive overview.

The EVM ecosystem is quite rich in this regard, with the OGs being GMX and DYDX. The new entrants making a lot of noise are Hyperliquid and Aark Digital. The Solana ecosystem is led by Jupiter and Drift Protocol.

You'll also notice the huge volumes generated by these platforms: between $1 billion and $10 billion in volume per week, which is almost equivalent to the DEX market volume which is the core vertical of all DeFi protocol.

How to explain this? It’s simple. To go back to our car example, the volume is counted not by the underlying asset (like in a spot market) but by the size of the bet. For instance, if I take a 10x leverage on a $1,000 position, the trading volume is equivalent to $10,000

Size

There are two ways to assess the size of the perpetual markets: through open interest and trading volume.

Open interest in perpetual futures markets represents the total number of outstanding orders placed by traders at various price points in the order book. It serves as an indicator of potential liquidity for the perpetual contract.

The term "potential" is crucial here, as it distinguishes this form of liquidity from that found in Automated Market Makers (AMMs).

Unlike AMMs, where liquidity is always active and readily available, the liquidity reflected by open interest is conditional.

It can fluctuate based on market conditions, price movements, and trader behavior.

Open interest provides a snapshot of latent market depth that may be activated as market dynamics evolve, offering insights into possible trading volumes and market sentiment.

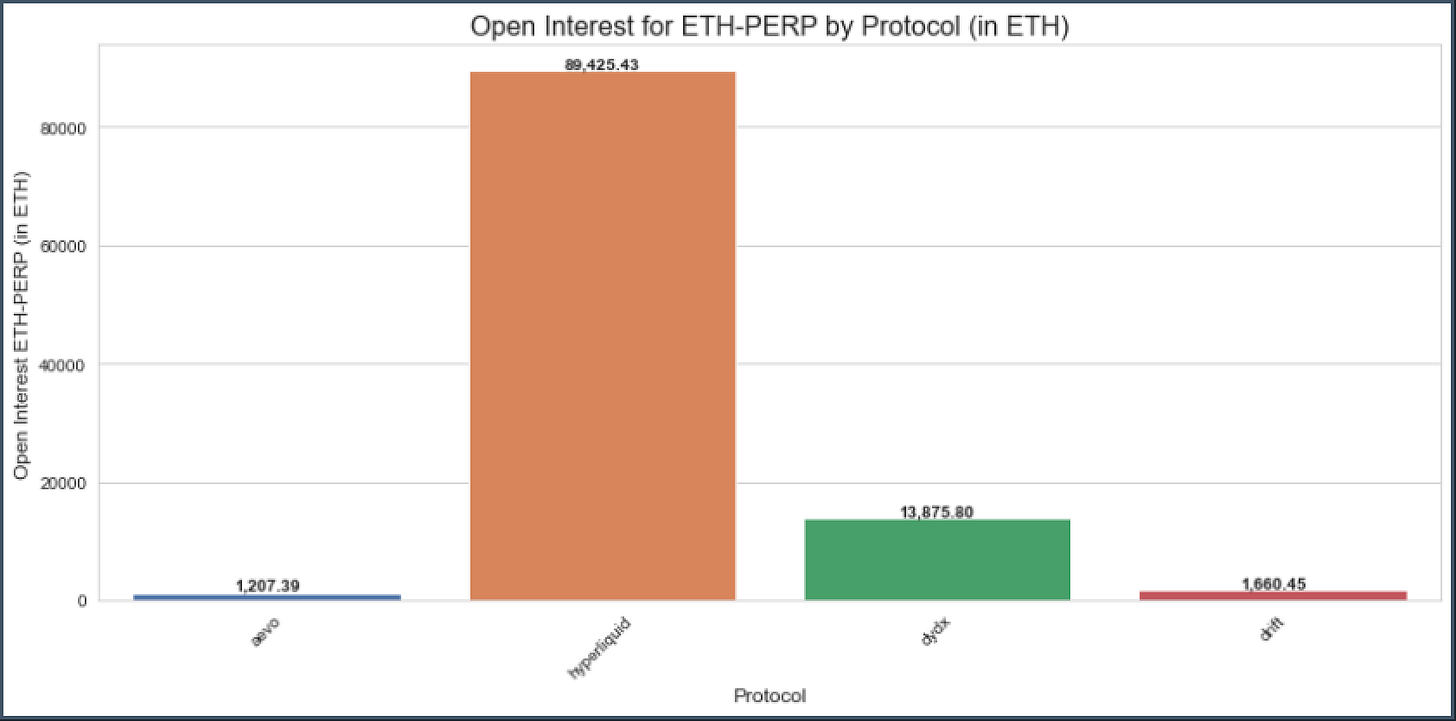

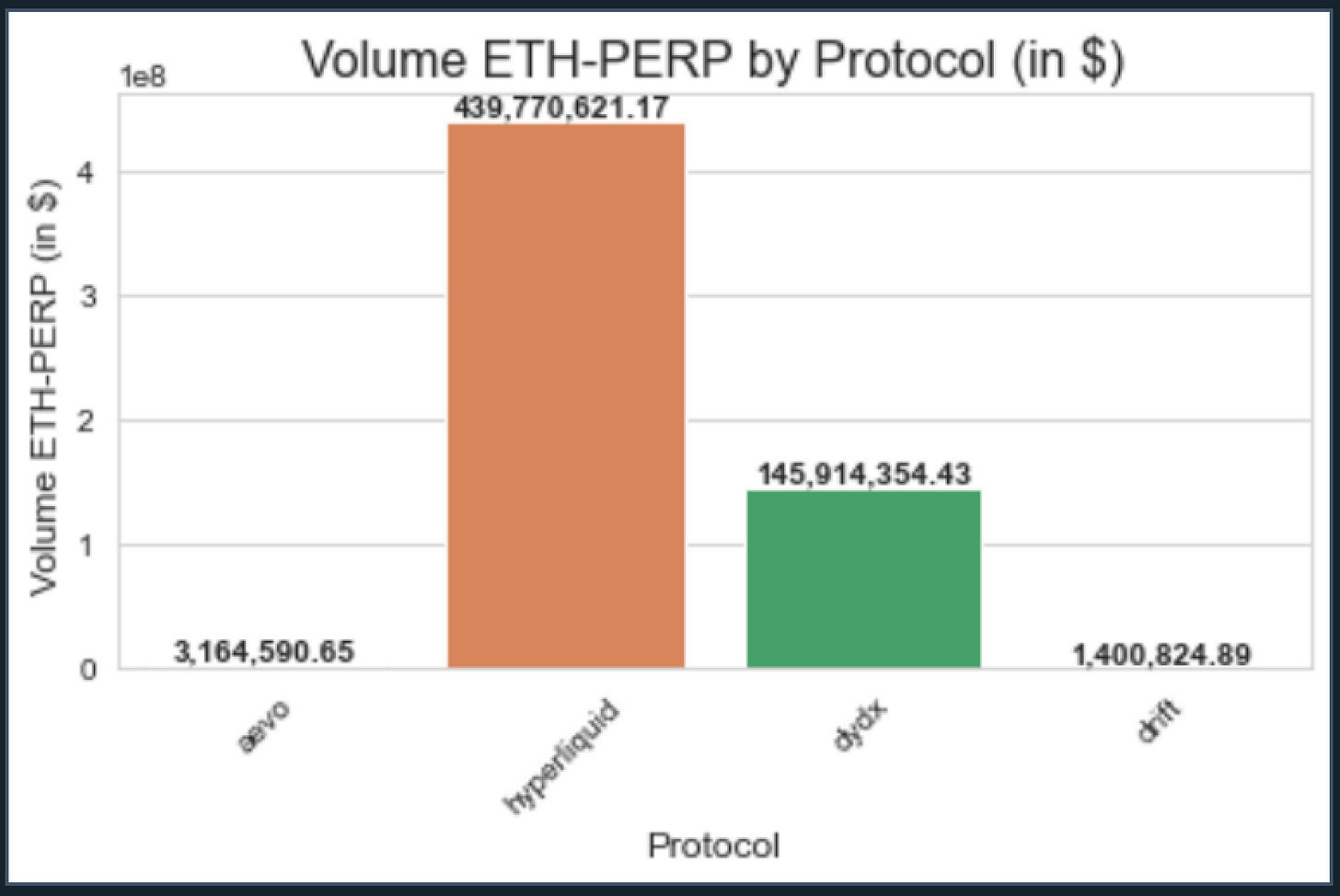

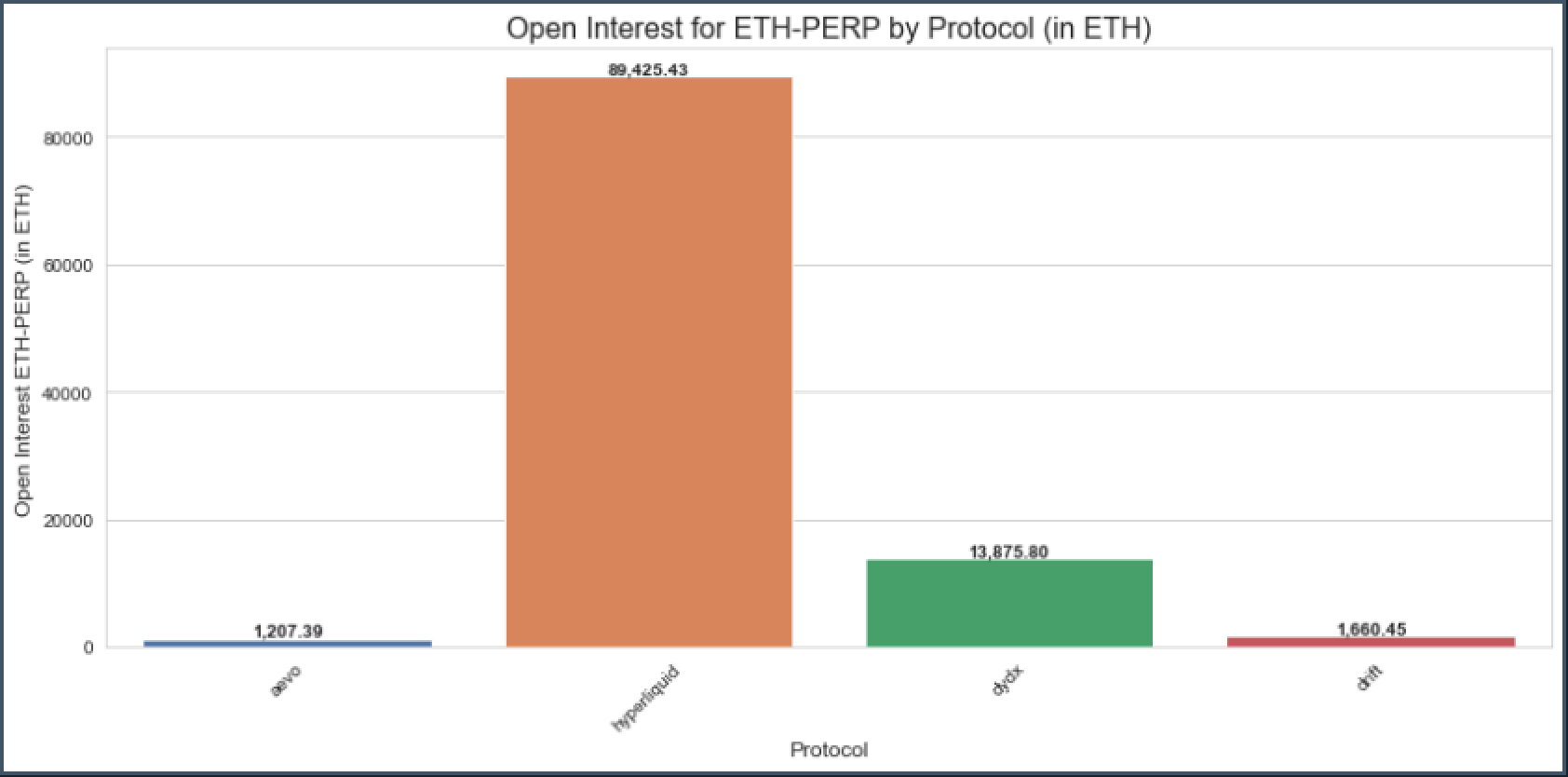

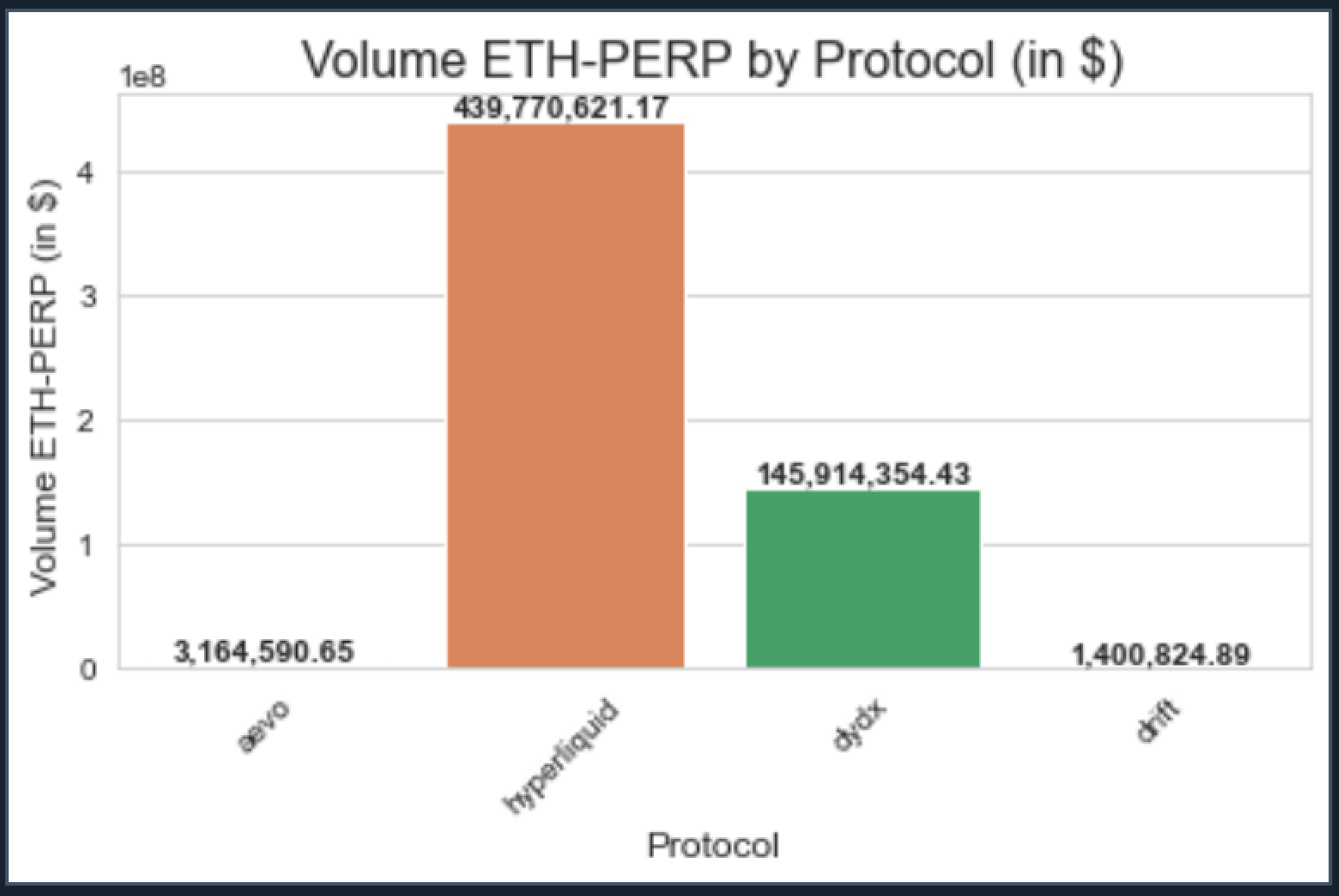

The range of open interests for the same market across several perpetual futures platforms is colossal.

On the ETH-PERP market, the size of open interests on Hyperliquid is 7 times larger than for DYDX, which is itself a fairly large market player.

On Aevo or Drift, the open interests are about 40 times smaller.

Trading Volume is obviously another interesting metric.

However, while this is the cardinal metric for spot markets and DEXs or DEX aggregators, it's somewhat less the case in derivatives markets. It's easy to inflate it by executing trades using very little collateral but with high leverage. Hence, there is the possibility of placing an order with very few assets.

Three curious observations

Few but super active users:

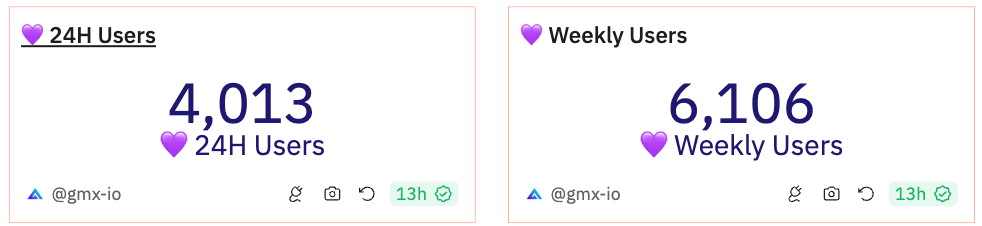

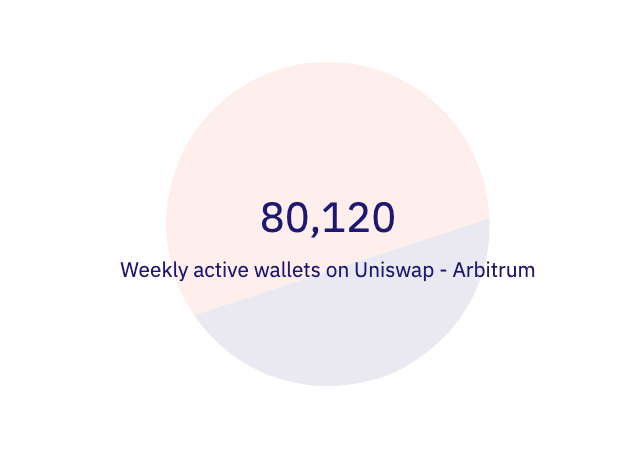

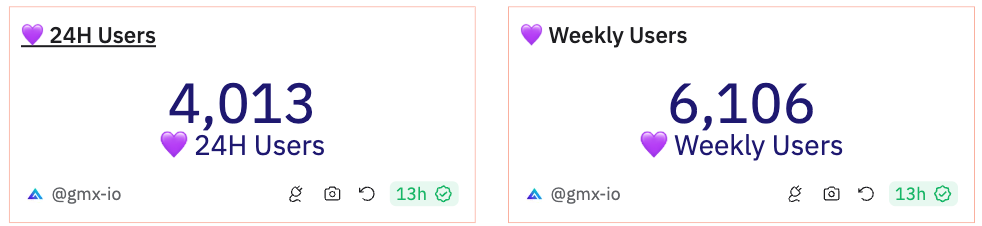

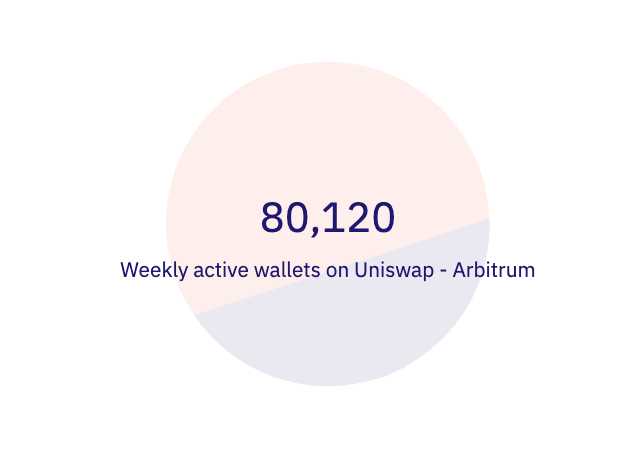

GMX vs. Uniswap on Arbitrum

The difference in a number of active addresses interacting with GMX is two orders of magnitude lower than Uniswap.

It explains how many genuine users populate DeFi as there are few incentives for perpetual users to hold several accounts.

In the last 7 days: 6,000 unique addresses interacted with GMX vs. 80,000 on on Uniswap.

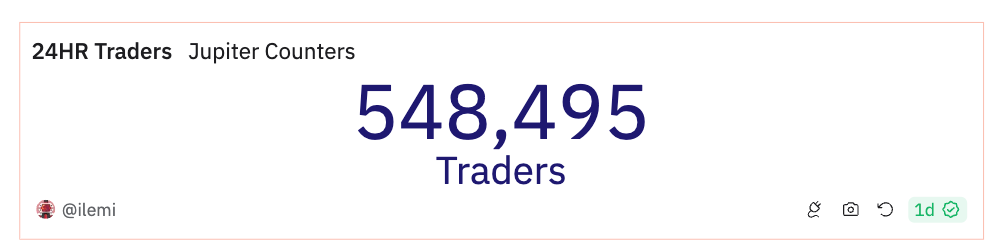

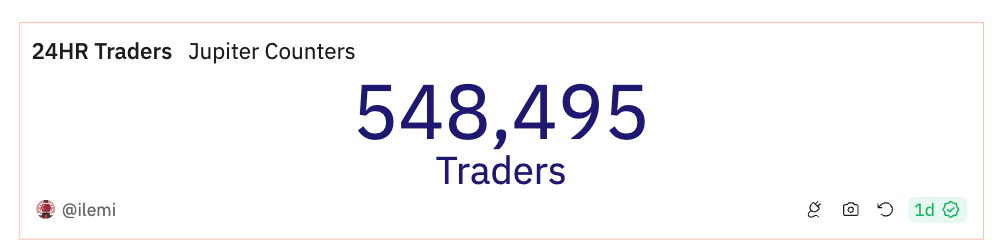

Jupiter swap traders vs. perp traders:

The same observation could be made on Jupiter. While 548,000 addresses interacted with the swap program in the last 24h, only 6,804 interacted with the perps, 100x less.

The reason?

The distinct natures of the two products as it is less time-sensitive to perform a swap than opening a position.

Also

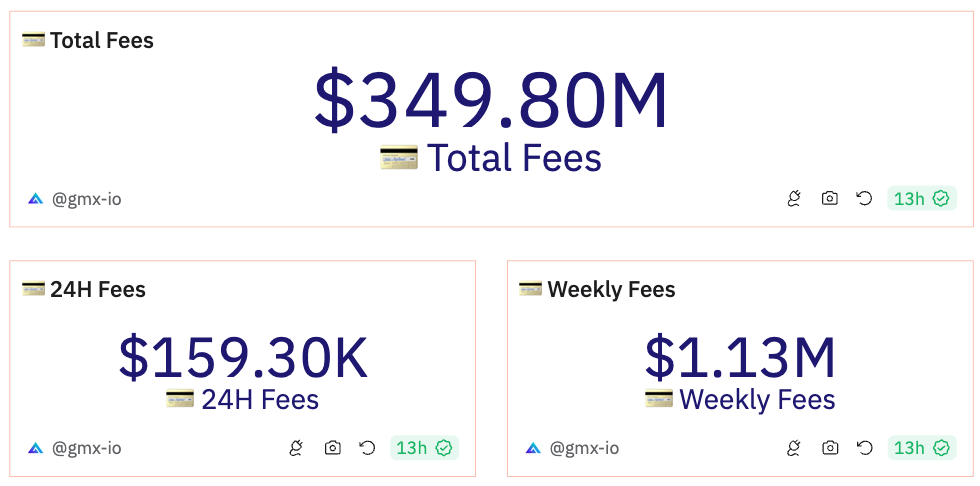

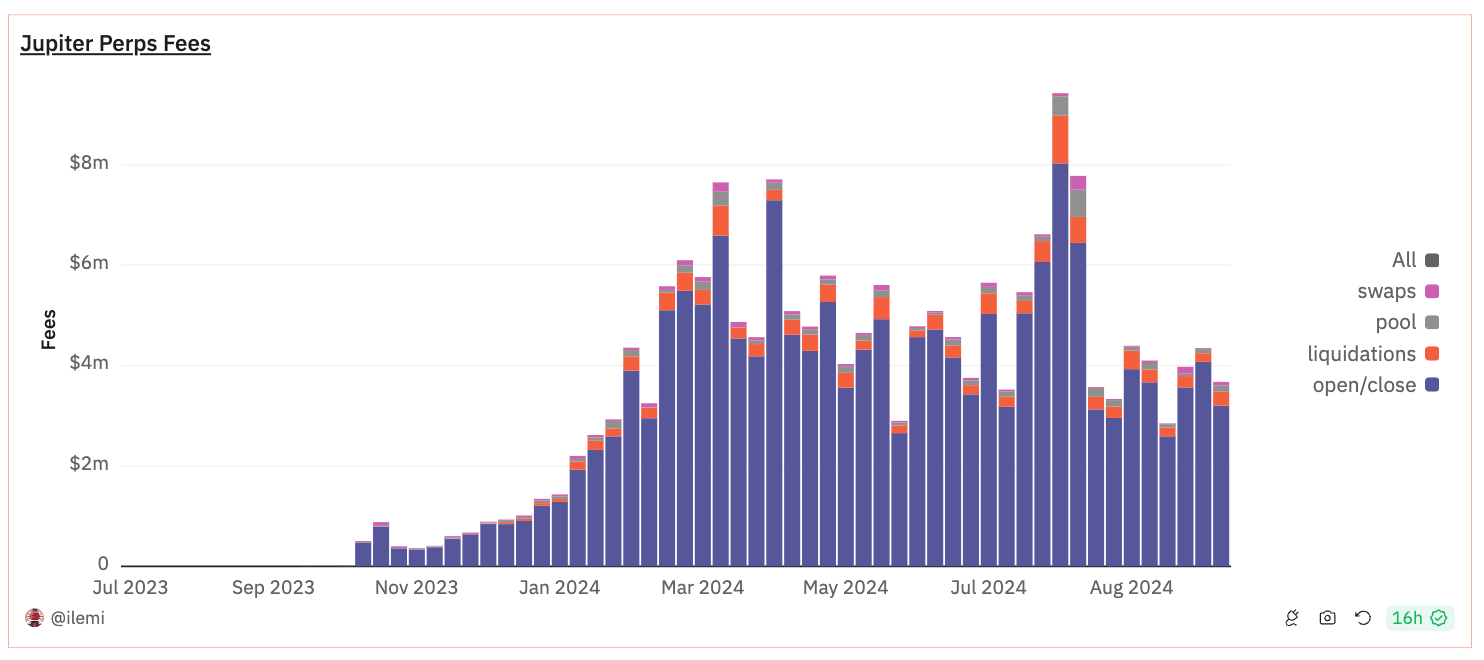

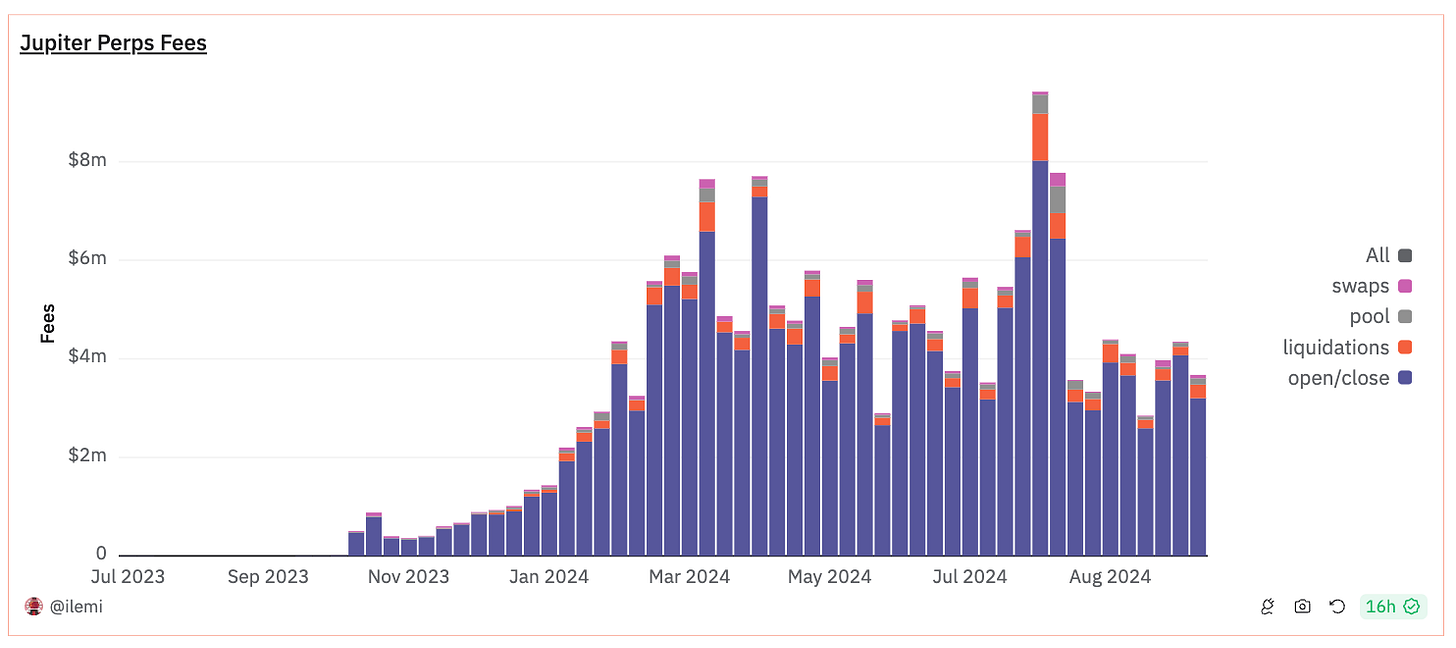

Cash machine:

Despite the low number of users, the fees generated are quite high, ranging from $100k to $300k per day on GMX (70% of which is redistributed to liquidity providers) and from $200k to $800k on Jupiter (also largely redistributed to liquidity providers).

How can users accept such fees?

Given that users' positions are often leveraged, with multiplied profit expectations, they are willing to lose a bit more on average per trade than capped positions.

In the mind of someone less risk-averse, it's easier to accept paying $2 in fees for a potential gain of $1,000 than paying $1 for a gain capped at $100, even if the average expected return is similar between the two positions.

The key role of iquidity Providers

A liquidity provider (LP) plays a key role in a perpetual protocol by supplying assets to the protocol's liquidity pool. Traders who want to open leveraged positions or make trades then use these assets to do so.In return for providing liquidity, LPs earn a share of the fees generated by the trades, along with other incentives, such as token rewards. Essentially, LPs help keep the market running smoothly by ensuring there's always enough liquidity for trades to happen, and they earn rewards as compensation for the risk of their assets being used in the protocol.

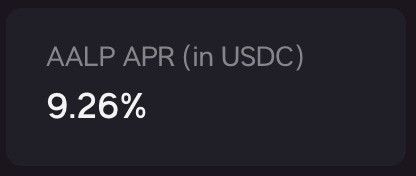

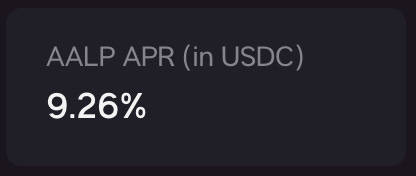

These actors play a crucial role in the stability of protocols.On Jupiter, JLP holders earn the equivalent of 35 to 40% annualized. It's around 7 to 11% for GLV holders on GMX and 9.2% for AALP holders (on Aark).

However, it's not easy to compare these yield rates, as they depend on the composition of each basket underlying these tokens, and especially on the fluctuation of fees earned from week to week.

Additionally, the underlying risk is highly differentiated and depends on the liquidation methods (and the oracles) used for user positions. This deserves a dedicated topic for discussion.